I think there will be a lot of pressure on them. Once they get to the point of refusing to write homeowners policies for most of rural California and coastal Florida, I think politicians will lean on them. Hard.

People thought that substantive action on climate change would have been too expensive. It certainly would have been expensive. But failing to take action was like making minimum payments on the credit card every month, and hoping that we would wake up one day and it would all be paid off.

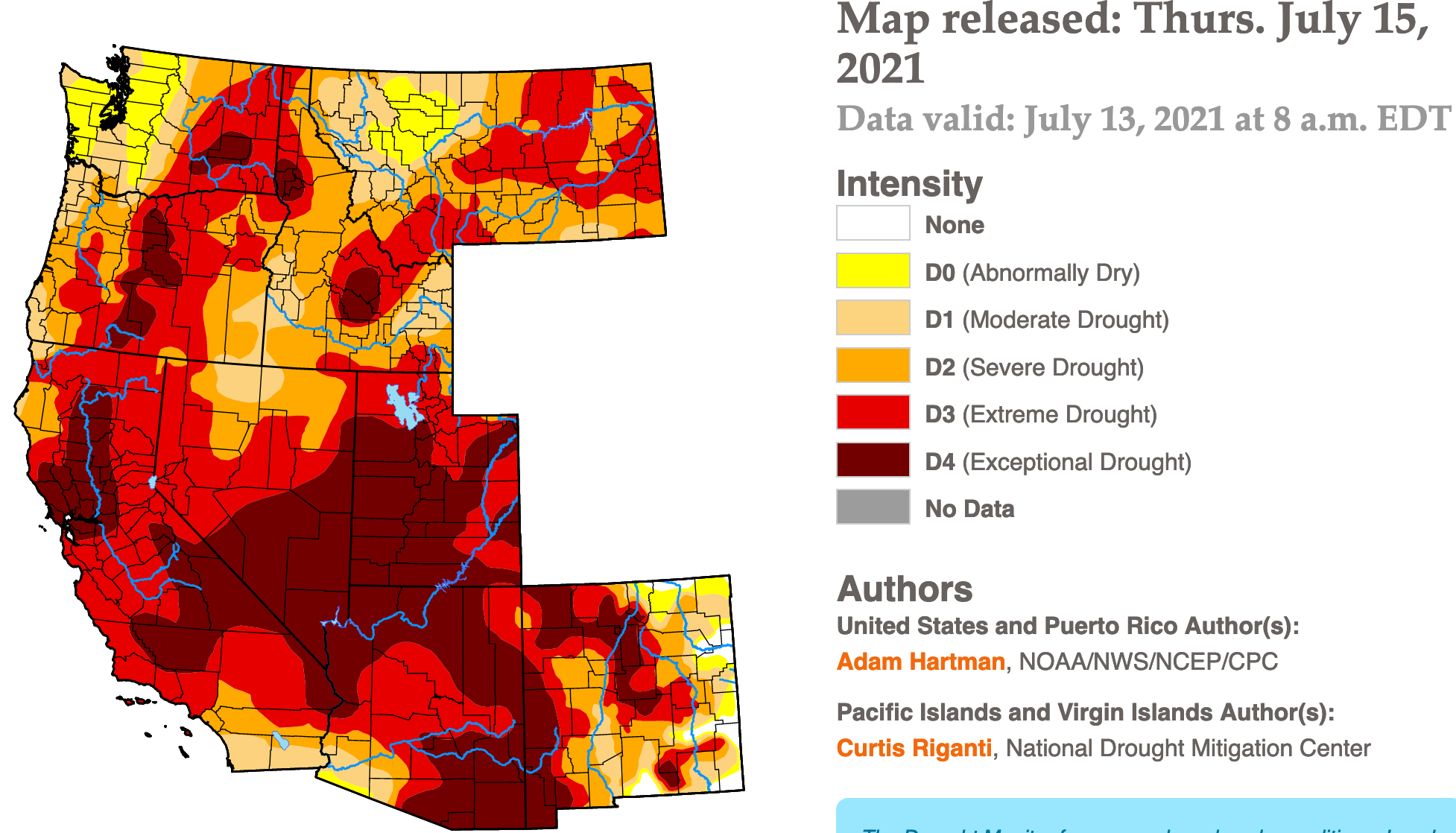

For sure there may come a time soon when politician will put pressure on insurers. But I think that’s still unlikely to trigger any form of advocacy for climate change measures from insurance companies.

I assume insurers will go on about how they are private companies and they have to ensure that they are ultimately profitable at the end of the day and how those particular groups don’t allow them to do so. Given the trend on the challenges to the health insurance individual mandate, I think many politicians will take that as an acceptable explanation and leave it at that.

We’re likely venturing into the questionable zone of the forum’s no politics rule here though if we continue, so I’ll leave it at that and hope Todd and the gang allow me some leeway here for this post.

If the businesses were structured properly, these older wineries ought to be sitting on massive numbers of different investments, any one of which could be liquidated if there were a need for cash to repair fire damage.

Unless of course for all these decades the businesses were run by boomers who ate the seed corn.

BTW, I’d be very interested in trying any White wines they chose to make from smoke-damaged Cabernet Sauvignon or Cab Franc or Merlot or Petit Verdot or even Zinfandel.

It’s terrible how much the world is shifting. I think it was dramatically evident in the 2000s when you had something like 3 or 4 “vintage of the century” in Bordeaux. And now we’re going past that. Will WA become the new Napa? And eventually Vancouver?

I love your wines, Jim, but I don’t know how you can stay in business making 10% of your production and the choices you need to make to stay afloat and employing your staff & crew (and yourself). I can’t imagine how tough these decisions are.

BTW - I had your '11 Etzel Block a few months ago. Absolutely fantastic. It’s evolved so much from when I last had it in 2014 and it really blew me away - was not at all what I was expecting. Thank you for the experience! Have one left.

I’ve heard that from a few winemakers - they wrote 2020 off, but could deal with the loss. But if it repeats again, it’s gonna get dicey. I’m praying it won’t for all of us but especially for you guys that have employees and vineyards to manage.

Last year has taught me more than perhaps all my previous years combined in life. Both personally and for my winery. And that is: keep the nut small. I’m so glad I only signed the lease for the smaller space and not the twice as big space I initially wanted. Yeah, it sucks to move everything around a million times and have no space for anything, but when the rent check gets sent every month it’s worth the pain.

This assumes that winemakers and wineries see their business purely as an asset. Knowing many, it’s not the case for the small and medium-sized ones. It’s a life.

Plus, you need to insure in order to sell and distribute. Insurers aren’t just making it difficult for wildfire loss - it’s coverage across the board.

Also, as noted, not every winemaker has hard assets to leverage. They need to insure their wines in storage.

Oh, and finally, what lender is gonna let its borrower remain uninsured? I don’t think many lenders think “oh, if there’s a loss, I’ll just let my borrower hand back the rest to me” is a wise underwriting strategy.

Non-remote scenario: When commercial insurance is cancelled or lapses, the lender can declare a material monetary default and thereby call the loan for immediate prepayment. However, the borrower may be unable to comply.

Which solves what? I don’t see what this has to do with the original point, which is that wineries across Napa and Sonoma are having serious trouble getting affordable insurance?

Well, fortunately for us 2019 was our largest volume vintage ever (difficult to do that year but we were working on moving up) and 2018 was not far behind so we have/had quite a bit of inventory to draw upon. We drastically reduced the offerings and allocations to distributors and are spreading out the sales of those two vintages over a longer period of time and selling an even vaster majority than normal (percentage-wise) through the club, tasting room and online. Also, fortunately, we were and are set up to do this. A lot of wineries are not either by circumstance or choices that didn’t involve a wine-ruining fire event. Hopefully the 2021 vintage is free of any such event and is relatively bountiful (from what I am seeing right now it is a highly mixed bag with some 2019 style of tonnage mix) and high in quality. We will have Tempranillo Rose and Sauvignon Blanc to bottle and sell in the spring and summer and 2021 vintage Pinots in the fall. Will it be some sort of banner year by the standards of our P&L? Assuredly not. Can we get by without some sort of company-changing impact? That’s the plan and the goal. I know that we are quite fortunate in a situation where the pain is spread around to literally every winery.

Glad for the report on the 2011 Estate Vineyard, Etzel Block. That vintage is drinking really nicely right now for those that enjoy that particular bent of wines. They have fleshed out quite a bit since their initial releases when they were far more wiry. An Estate Vineyard, Bonshaw Block opened at the tasting room yesterday was similarly well-received.

We’re in a position along the lines of PGC, except for the bountiful 2019 aspect. However, our staffing is two people on salary, so we have a better than average ability to hunker down and control costs.

That said, while we may release some 2020 wines, it will be at most 40-50% of normal, and I do not expect to release them on schedule(and probably not at normal pricing regardless of quality). Next year will be a good year to pick up library wines from Goodfellow, because that’s what we’ll have to sell.

But as Jim said, if smoke arrives again this year, it’s unlikely that we will have a solution.

That’s precisely my point - you’re required to purchase insurance if you’re leveraged.

But if you’re self-financed, then frankly you don’t really need any insurance at all [particularly not if you’re familiar with this Australian invention called “Hardipanel”].

The bottom line actuarially is that almost everyone almost never needs insurance [otherwise either the insurance companies would quickly go bankrupt, or else the taxpayers would almost as quickly go bankrupt from bailing out the insurance companies].

To me, what the article seems to be hinting at is that a whole lot of these celebrity Napa wineries were financed with OPM.

I have earthquake insurance in addition to fire.

I raised my deductible on “named” fire as my warehouse location is fairly unlikely to burn, but I am in a “dangerous” zip code.

My rates are silly, but I am insured at the moment.

Deep down my concerns are whether the insurance company would pay in the event of a catastrophic loss.

I recently talked about this with our insurance agent. I’m actually most worried about damage from fire caused by a quake, which I was told is not covered by normal fire insurance. Something to make sure you have enough quake coverage for.