Another noodle-slinger? ![]() But a successful one!

But a successful one!

To the extent Bdx prices actually are dropping (and I am seeing it with 2019 EP), I’d hazard a guess it’s solely a result the tariffs situation; many (most?) 2019 EP prices do not have tariffs built-in, so one should reasonably add 25% to the current price to get to the probable final price.

Does anyone have a sense of how important removal of these tariffs would/will be to a potential Biden administration? Given all the other things going on in our country, and the world, I find it hard to believe removing these tariffs is going to be anywhere near the top of the priority list … I think we may be stuck with these for awhile, but would love to hear conflicting viewpoints/news/opinions.

With few exceptions, all 2018 were bottled a few months ago

Aite. They’re still uniformly ‘EP’ with my merchants, but I’m pleased to hear that. Will be hard to resist popping an early 18 Pontet Canet. Think the only physical I have is the 18 Ygrec d’Yquem

Several reasons

Between 2014 and 2020, 17 is the weakest vintage.

Covid

Tariffs

Brexit

It’s more of a European styled, classic year.

16 and 18 are both knockout vintages.

2019 was well priced and killed off what little demand there was for 2017. Better wines for less money will do that.

They are pre-arrival, not EP. EP for 18 was 19.

Sure, whatever the terminology is. My point is that simply none of them (except the Y d’Yquem) are in London yet. In my simplistic view of the world, they’re en primeur untill a decent volume hits my local market and is immediately availablle

I would add that, IMHO, the Chinese market for trophy wines from Bordeaux is down due to an apparent crackdown on corruption, which apparently often took the form of trophy wines being “gifted” in lieu of actual cash. And Chinese buyers were a big piece of the market approximately five years ago.

And correct me if I’m wrong, but wasn’t there a lot of hand wringing about 15, 16, 17 being way overpriced when they were offered EP? Maybe those opinions were correct and at least some buyers were, marginally, priced out of the market.

I think this is key. Distinguishing between EP pricing and market pricing for Bdx. The chateaus might have overshot their EP pricing given the various headwinds mentioned but market pricing across a broad set of Bdx vintages is flat (maybe up a tad?) since 2017.

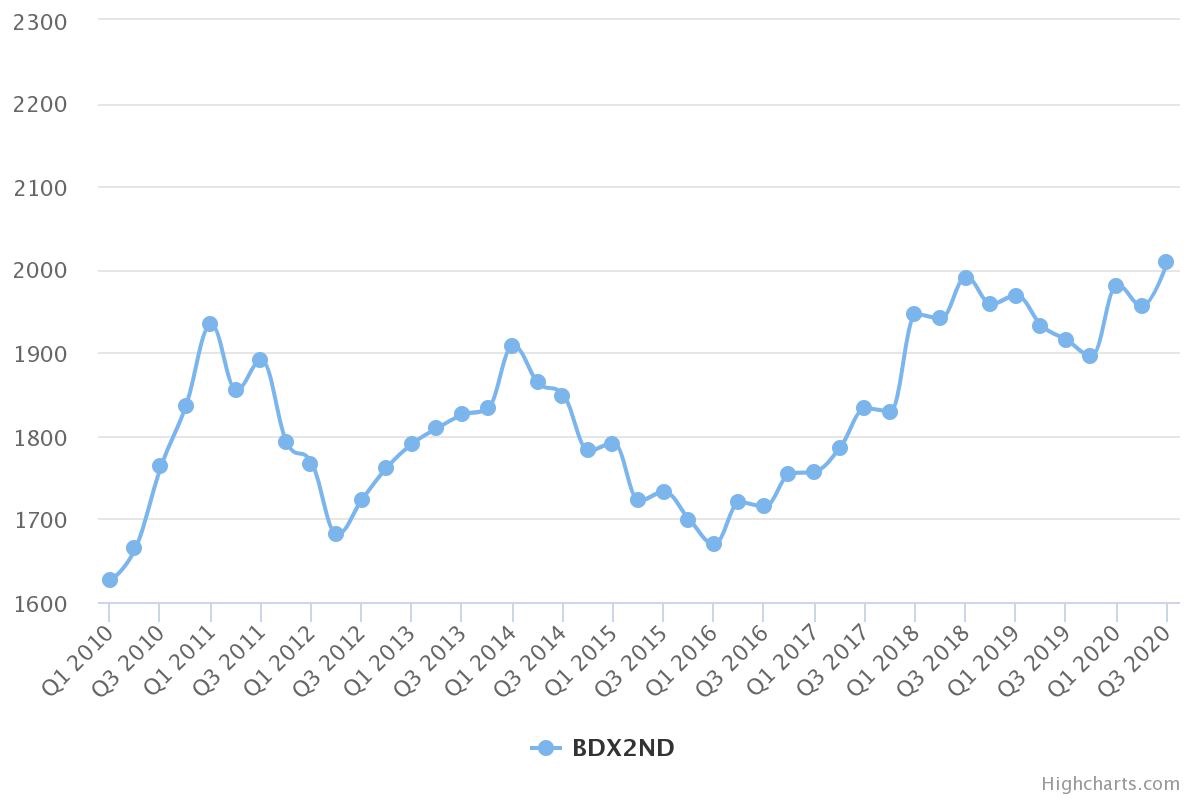

Here’s the 5-year Bordeaux Index from WMJ. Represents five highly regarded and actively traded modern vintages of twenty chateaux often referred to as the ‘super-seconds’. The vintages in the index are 1989, 1990, 1995, 1996, 2000, 2005…index has risen from a value of 1757 in q1 2017 to a value of 2009 today. So about a 15% gain. The first growth index is only up about 5% over that same time period, and is relatively flat compared to 10 years ago…owing methinks to their Uber high prices that settled in around 2010.

Tariffs are causing US prices to go down??? ![]()

I assume was what mean is that the Bordelais set a lower EP release price in anticipation of the possible tariffs the buyers would have to pay on delivery?

I think that been a factor with 2019 releases, but there is a slew of other stuff which seems to have weakened Bordeaux. I think we have touched on all of them here, but the single greatest factor is simply supply and demand. Supply is up, way up, and demand is relatively weak.

The other problem for the Bordelais is that their prices make opening a bottle pretty much a special occasion choice. Yes, I can find wines under $30, but if I want a bottle of a minor classified growth like Branaire or Issan, prices have gone up about 100%, while the steak that I am eating with it less than 20%.

I wonder about the accuracy of these indexes. For example, I documented in the “Wine pricing bubble” thread that the current prices of 2010 first growths are now 25% below their first tranche futures release prices, that before any inflation adjustment, and that 2016 release prices for first growths were one-third lower than the 2010 release prices. That doesn’t seem very compatible with first growth prices being “relatively flat” over the last ten years. You can do a lot with an index by picking your vintage years carefully, how you weight it, etc.

As Mark says, Bordeaux faces a supply and demand problem from hell. Good vintages do a lot more to boost the supply problem than anything they do in terms of increasing demand, it’s more that bad vintages depress demand even more rather than good vintages increasing it. It’s actually pretty impressive what they have been able to do in terms of maintaining prices in the face of so much excess supply. They have managed to stabilize super seconds prices for hyped vintages in the $150 range, and solidly above $100 for the non-hyped ones when for a while there it looked like they could start dropping below $100. I mean, when you think about all the great wine out there in the world it’s pretty amazing that, say, the 2013 Ducru Beaucaillou (to take a random example) sells for $120+ a bottle. That is Champagne-level pricing and branding mastery.

I think it helps Bordeaux that their only real global competition in the cabernet blend category is Napa, which is probably the most massively over-inflated wine region and doesn’t market well on a global scale. There is also Argentina etc. but it doesn’t seem to be able to make the leap. (People ITB may correct this, just my impression).

Yes. Because we are not buying the wine, there is less demand and stock is accumulating. That is for 2017.

In 2019, wines were priced lower to help sell through as 25% is a massive up charge fee US buyers are willing to pay.

On top of Patrick’s opinion, I will just add that a big percentage of the newly released trophy Bordeaux are consumed during business dinners, and for those Chinese buyers who are into the wine, they are not buying Bordeaux EP to the cellar for ten or twenty years, it is much cheaper to just buy aged OWC from Hong Kong.

Based on my observation, the younger generations in China are losing interest in Bordeaux because it is hard to have access to “Normal retail price”, the wine retail store in the mainland usually charges 2-3x Winesearcher price for Bordeaux. For those who can afford that kind of price, they chose Burgundy. Based on what I saw frequently, collectors are willing to pay 500 USD to buy a Bizot village, but no longer willing to pay 500 USD for Lafitte. Just my 2cents.

Are there a lot of wine collectors in China? (I.e. people who accumulate hundreds of bottles to store for decades). It is relatively uncommon even in the U.S. which I think of as a stronghold of the collector culture, how common is it in Asia? Sorry if this is a very elementary question, I’ve never lived in Asia.

There are a ton of reasons…

EP campaigns no longer offer value

Younger generations drink less

Younger generations don’t cellar wines

Massive back log of wines in European warehouses

They make a ton of it every year

It’s not Burgundy or N. Rhone: it’s off trend

Tariffs

Price increases in general since 2000 vintage

Its sorta too bad as the wines, white and red, are better than ever from $10 to $3000 a bottle, but the Bordelais did this to themselves, they know how to fix it, be less greedy.

this is the big one for me to be honest - you see the price movement on the sceondary market as wines go to their prime windows. I think first growths, etc, you’re basically expecting scarcity in the short term to drive pricing, think Mouton as a really good example of that in the 2019 EP campaign. It’ll be fairly steady until it hits prime, and if it fulfills the promise when it does hit prime, it could get to quite a nice spot.